By choosing our financial budgeting services, you can get a budget that's tailored to your particular needs.

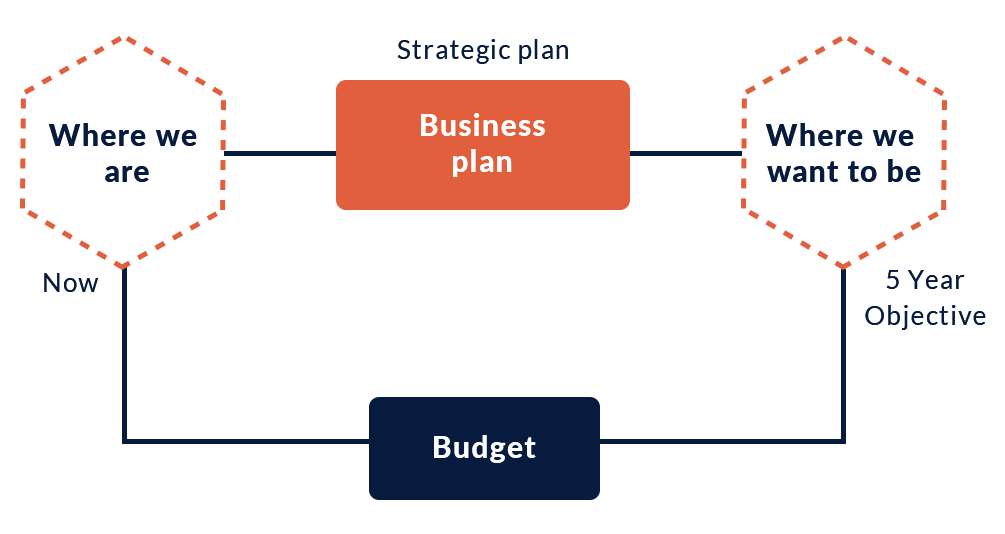

Budgeting is the tactical implementation of a business plan. To achieve the goals in a business’s strategic plan, we need a detailed descriptive roadmap of the business plan that sets measures and indicators of performance. We can then make changes along the way to ensure that we arrive at the desired goals.

A robust budget framework includes an operating budget, a capital expenditure budget, and a cash budget. Combined budgets produce budgeted income statements, balance sheets, and cash flow statements.

Income, salary, benefits, and non-salary expenses are among the day-to-day operating expenses. Operational budgets are used by companies to plan their activities over time, typically a quarter or a year.

Typically, capital budgets are requested for the purchase of large assets such as property, equipment, or IT systems, which place a heavy strain on a company's cash flow. In capital budgets, funds are allocated, risks are managed, and priorities are set.

The cash budgets of businesses provide an explanation of how payments are made and how revenue is received. Management can assess the magnitude of additional capital and financing needed by using an effective cash budget.

Almost all large companies begin the budgeting process four to six months before the fiscal year begins, while some may take an entire fiscal year to finish. Monthly budgets and variance analyses are the norm in most organizations. To finally implement the budget, the company follows a series of steps starting with the initial planning. In addition to communication, various processes include setting objectives and targets, developing a detailed budget, assembling and revising the budget model, and reviewing and approving the budget.

Mr Desai takes the time to learn about you and your financial goals and simplifies complicated financial information, making it even more enjoyable! Following a few meetings with him, our financial lives became more ordered and our road forward became crystal obvious. We’ve accomplished more than we anticipated because to her strategic analysis, financial planning fluency, and direction. I’ve already referred him to a few friends. Collaborating with the Uppscalle team is similar to having an expert, coach, and cheerleader all rolled into one.

In 2019, my wife and I met Amit. We knew how to earn money and how to spend it, but we were novices when it came to financial planning. Following our discussion with Amit, we implemented their recommendations, and here we are in 2022, incredibly satisfied with our choice. We find the entire Uppscalle crew to be friendly and easy to work with at all times. They are constantly accessible, friendly, and helpful, and they are quite easy to suggest.

Passion, knowledge and a genuine interest in achieving the best for clients is what makes a truly professional Financial Adviser. Uppscalle has this and more. Their dedication to clients, business excellence and education sets them apart and I would highly recommend them to anyone wanting to achieve better financial outcomes.

I’d like to convey my gratitude for the effort they’ve done on my behalf over the years. They have handled my financial issues with unmatched professionalism and attention to detail. The certainty I have in the total integrity of your dealings with us is particularly encouraging. Your constant counsel on financial planning matters has resulted in significant financial savings for us. May you and your clients flourish.